BlogThe Real Cost of a Wrong API Example in Financial Services

A wrong code example in a payments API doesn't post the wrong image — it moves real money. Here's why fintech API docs need the same rigor as transaction processing, and what the best platforms do about it.

A developer copies a code example from your API docs. Changes the account ID. Updates the amount. Hits send.

The money moves. To the wrong account. Using a deprecated endpoint your docs still show as valid.

In a social media API, a wrong code example posts the wrong image. Embarrassing. Fixed in seconds. Nobody loses sleep.

In a financial services API, a wrong code example moves money. And "Ctrl+Z" is not a feature that banking infrastructure supports. Reversing a bank transfer isn't a rollback — it's a new transaction that requires the receiving party's cooperation and days of processing.

Let me be blunt: wrong API examples in fintech aren't documentation bugs. They're operational incidents waiting to happen. The only question is when.

The Numbers Behind the Problem

Code examples are the most critical — and most fragile — part of API documentation. The data makes this uncomfortably clear:

- 75% of production APIs have variances from their OpenAPI specifications. Not minor style differences — actual behavioral drift between what the docs say and what the API does. (Nordic APIs / APIContext)

- 70% of developers rate code examples as the single most important component of API documentation — above reference docs, above tutorials, above everything else. (SmartBear 2020 State of API Report)

- 55% of teams struggle with inconsistent or outdated documentation, with context fragmented across Slack, Confluence, and email. (Postman 2025 State of the API Report)

- 83% of developers consider documentation quality when evaluating whether to adopt an API. 71% have chosen one API over another specifically because of superior documentation. (Monetizely)

So: three-quarters of APIs don't match their own docs. The thing developers trust most in those docs is code examples. And documentation quality is the deciding factor for the majority of API adoption decisions.

In fintech, this isn't an inconvenience. It's a liability with dollar signs.

Why Code Examples Go Wrong (And Why It's Inevitable)

API documentation doesn't go stale evenly. Conceptual guides and tutorials drift slowly — they use general language that stays roughly accurate even as the product evolves.

Code examples break fast. They contain specific endpoints, parameter names, field values, and response formats. When any of those change — and in an actively developed API, they change constantly — the example either stops working or, much worse, works but does something different than what the developer expects.

That second scenario is the one that should terrify you.

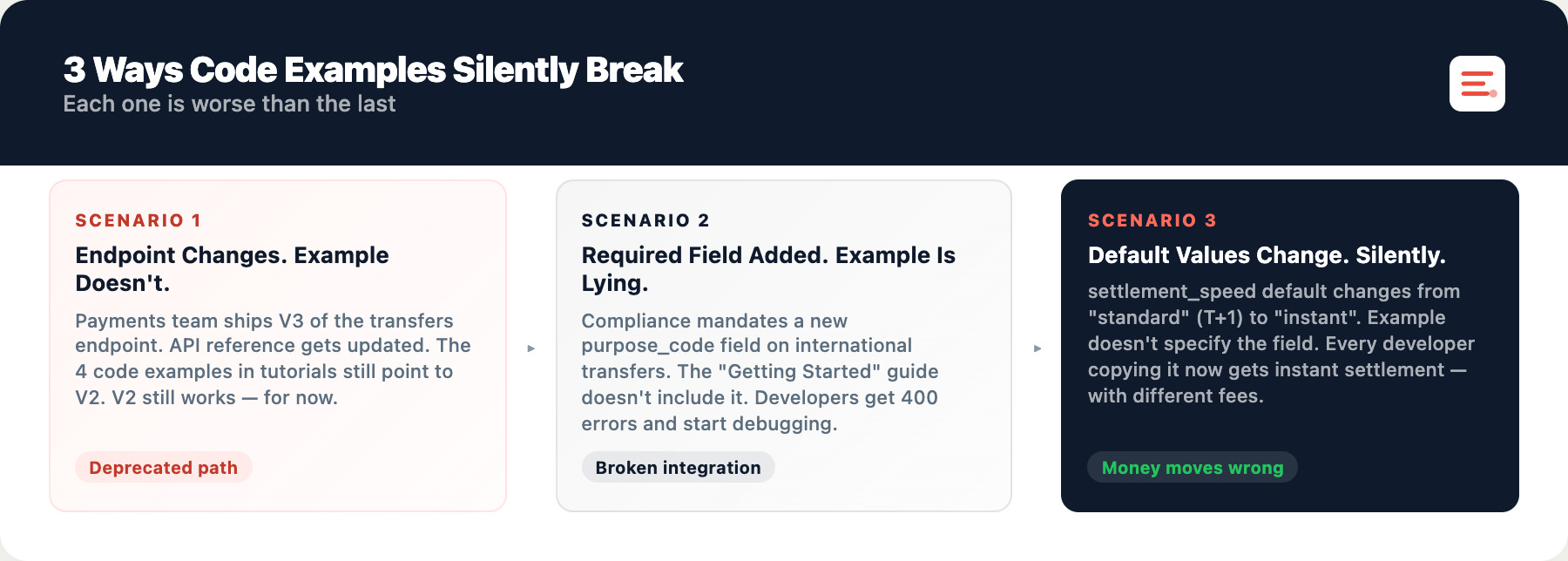

There are three ways this plays out, and each one is worse than the last:

The endpoint changes. The example doesn't. Your payments team ships V3 of the transfers endpoint. The API reference gets updated. The four code examples scattered across your quickstart, integration guide, and two tutorials still point to V2. V2 still works — for now — so nobody notices. Meanwhile, a developer builds their entire integration on a deprecated path.

A required field gets added. The example is suddenly lying. Your compliance team mandates a new purpose_code field on international transfers. The API now rejects requests without it. But the code example in your "Getting Started with International Transfers" guide doesn't include it. A developer copies the example, gets a 400 error, and starts debugging.

Default values change. Nobody tells the developers. This is the one that makes my stomach drop. Your API used to default settlement_speed to "standard" (T+1). A product update changed the default to "instant". The code example doesn't specify the field because "the default is fine." It's not fine anymore. Now every developer who copies that example is getting instant settlement — with different fees — and doesn't know it.

This isn't theoretical

A detailed post-mortem of PayPal's API documented endpoints listed in the official docs that simply didn't exist, webhook delays that went unmentioned, and aggressive session timeouts that forced merchants to discover limitations through trial and error — in production, with real transactions.

And it's not just fintech. When deprecated endpoints get forgotten in documentation, the consequences compound over time. In one healthcare case, a deprecated SOAP endpoint remained accessible for six months while vulnerabilities were only patched in newer REST services. The old endpoint was forgotten in the documentation. By the time it was discovered, 450,000 patient records had been exposed.

The Cost Isn't Developer Frustration. It's Everything Else.

When a developer hits a wrong code example in a non-financial API, the cost is time. They debug, find the issue, work around it. Annoying, but contained.

In financial services, the costs don't add — they compound:

Money moves. If a code example sends a test transaction to a production endpoint — because the docs don't clearly distinguish sandbox from production URLs — actual funds transfer. This is a persistent, documented problem across payment APIs. Failed payments alone cost the global economy $118.5 billion annually. And wire transfers cannot be reversed once processed — even ACH returns carry $15-$35 in fees per transaction.

Compliance exposure. Over 60% of fintechs incurred compliance penalties of at least $250,000, with a third paying over $500,000. TD Bank paid $3.09 billion after eight years of documentation/monitoring failures that enabled $600 million in money laundering.

Trust damage. 71% of developers have chosen one API over another due to superior documentation. Developers who successfully implement during evaluation are 3.7x more likely to convert. A broken quickstart example eliminates that multiplier.

Support escalation. Financial services average $300,000+ per hour in API-related downtime costs, with 91% of mid/large enterprises exceeding this.

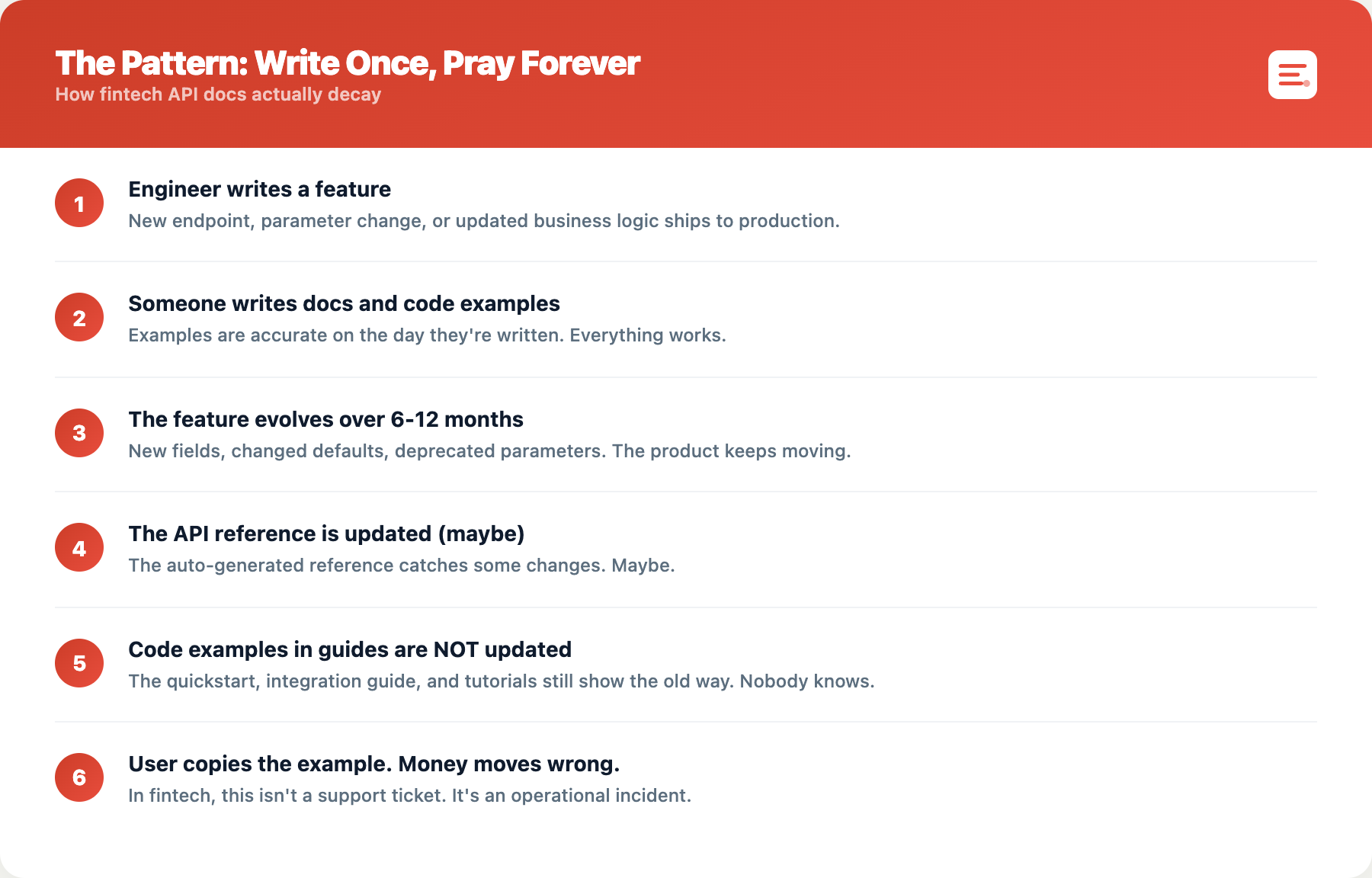

The Pattern: Write Once, Pray Forever

Here's how fintech API documentation actually works in practice:

Here's how fintech API documentation actually works in practice: An engineer writes a feature, someone writes the docs and code examples, and on the day they're written, everything is accurate. Then the feature evolves over 6-12 months. The API reference gets updated — maybe. But the code examples scattered across guides and tutorials? Almost certainly not.

The scale is measurable. Fintech teams experience 3+ payment failures per month from unannounced API changes — each costing ~$50,000. That's $1.2 million per year per organization. And 76% of failed API integrations result from inadequate documentation or support.

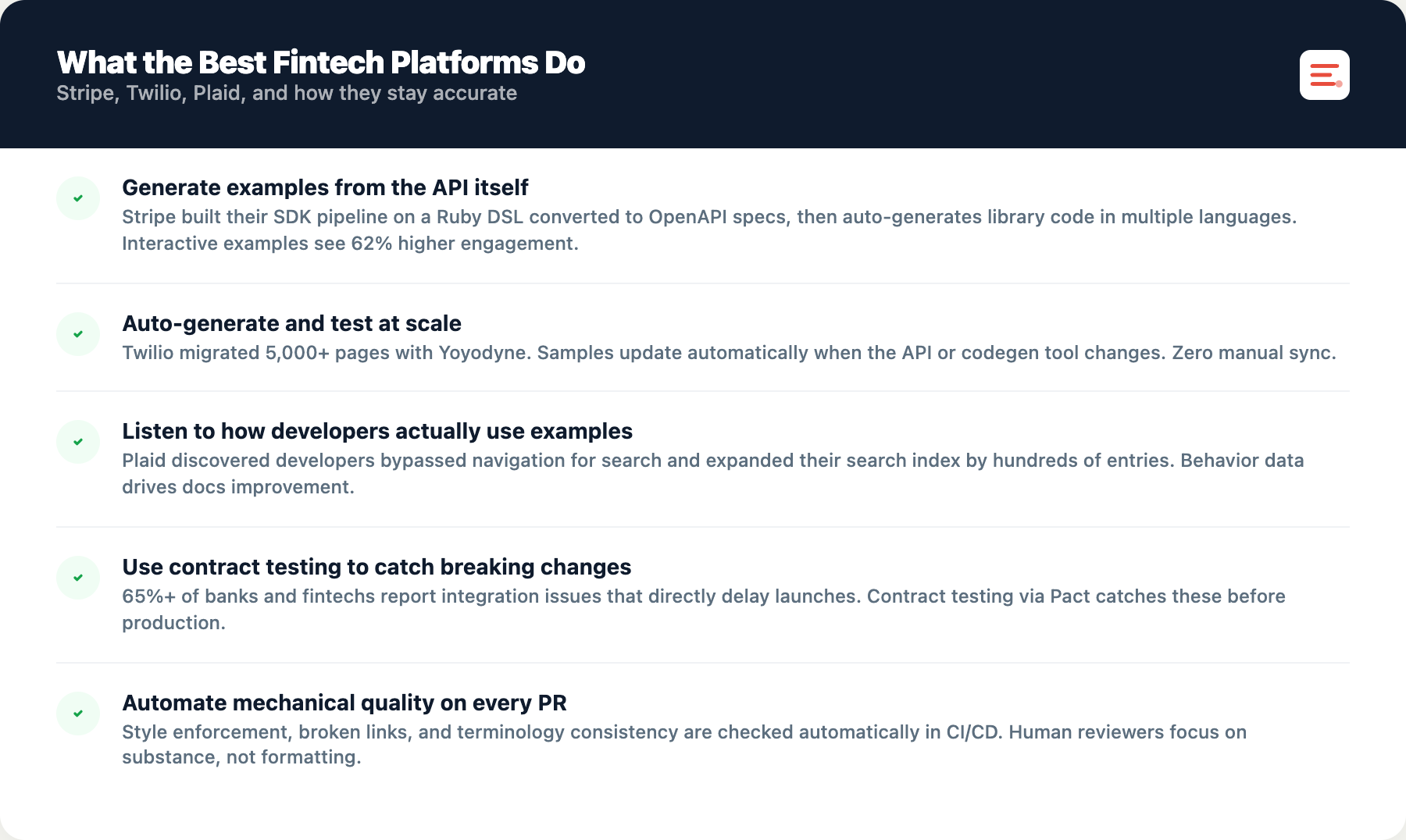

What the Best Fintech Platforms Do

They generate examples from the API itself

Stripe built their SDK generation pipeline on a Ruby DSL converted to OpenAPI specs, then auto-generated library code in multiple languages. They also built and open-sourced Markdoc. Result: interactive examples see 62% higher engagement.

They auto-generate and test at scale

Twilio migrated 5,000+ pages with Yoyodyne — samples update automatically when API or codegen tool changes.

They listen to how developers actually use examples

Plaid discovered developers bypassed navigation for search and expanded their search index by hundreds of entries.

They use contract testing

Over 65% of banks/fintechs report integration issues directly delay launches. Contract testing via Pact catches breaking changes before production.

They automate mechanical quality

Tools like Vale (open source) or EkLine (managed, CI/CD integrated) handle style, links, and terminology automatically on every PR.

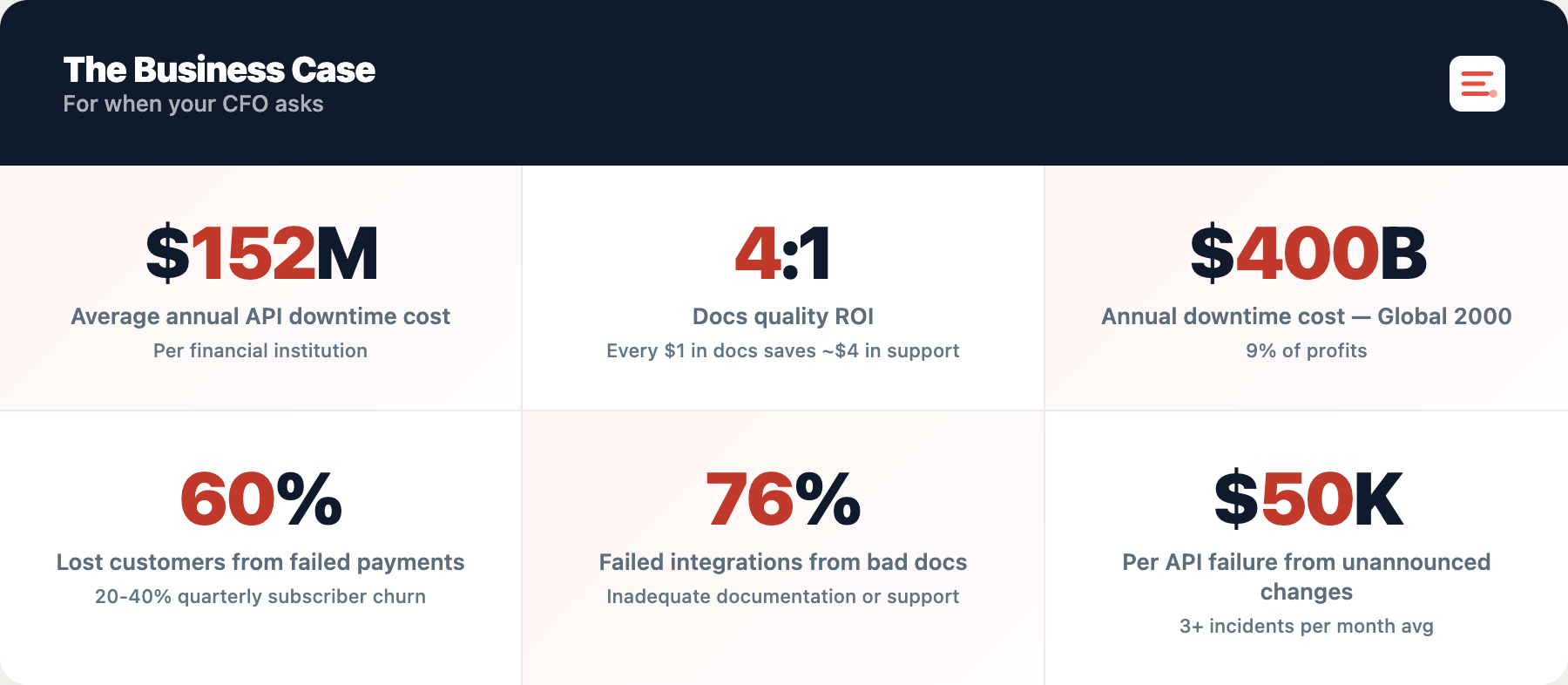

The Business Case (for When Your CFO Asks)

- API downtime costs financial institutions $152 million annually on average

- Every $1 in docs quality saves ~$4 in support costs (Monetizely)

- Downtime costs Global 2000 companies $400 billion annually — 9% of profits

- 60% of organizations lost customers due to failed payments; 20-40% quarterly subscriber churn

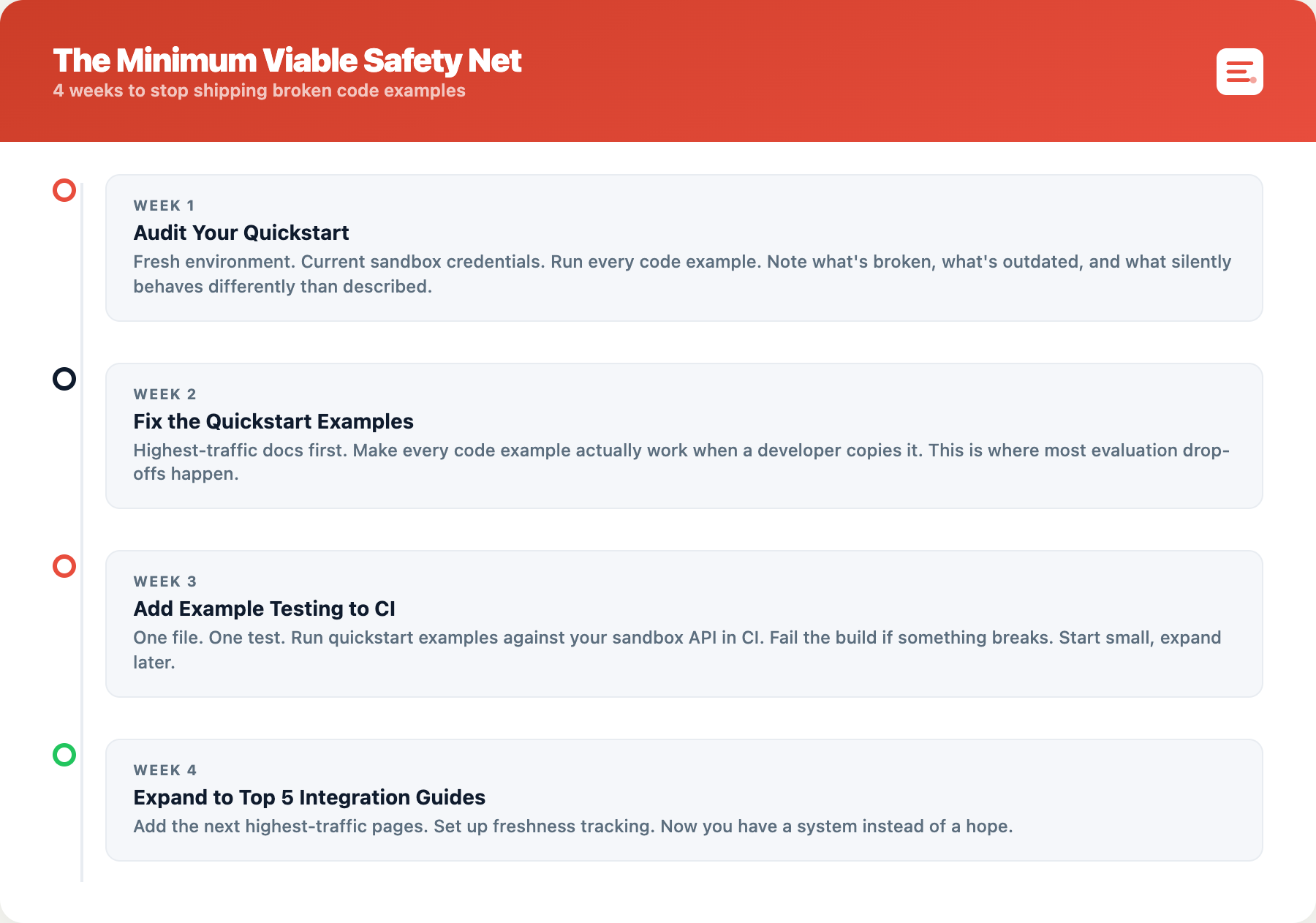

The Minimum Viable Safety Net

Week 1: Audit your quickstart. Fresh environment. Current sandbox. Note what's broken. Week 2: Fix the quickstart examples. Highest-traffic docs. Make them work. Week 3: Add example testing to CI for the quickstart. One file, one test. Week 4: Expand to top 5 integration guides. Set up freshness tracking.

"Mostly Right" Is Not Right

In most software, documentation that's 95% accurate is fine. In financial services, the 5% that's wrong is where someone loses money.

Your code examples are the most copied, most trusted, and most fragile part of your documentation. In fintech, they're also the most consequential. Treating them as testable, versionable, maintainable code — instead of as static text in a Markdown file — is the difference between documentation that works and documentation that creates incidents.

Outdated docs isn't a typo. It's a bug. And in fintech, that bug moves money.

We'll be at the Fintech Meetup at the end of March. If you're building a fintech developer platform and any of this hit a nerve, come talk to us about code example testing, documentation freshness, and keeping API docs honest. ekline.io or support@ekline.io.